If we want to find a stock that could multiply over the long term, what are the underlying trends we should look for? One common approach is to try and find a company with returns on capital employed (ROCE) that are increasing, in conjunction with a growing amount of capital employed. This shows us that it’s a compounding machine, able to continually reinvest its earnings back into the business and generate higher returns. And in light of that, the trends we’re seeing at Nextracker’s (NASDAQ:NXT) look very promising so lets take a look.

Understanding Return On Capital Employed (ROCE)

Just to clarify if you’re unsure, ROCE is a metric for evaluating how much pre-tax income (in percentage terms) a company earns on the capital invested in its business. To calculate this metric for Nextracker, this is the formula:

Return on Capital Employed = Earnings Before Interest and Tax (EBIT) ÷ (Total Assets – Current Liabilities)

0.36 = US$587m ÷ (US$2.5b – US$891m) (Based on the trailing twelve months to March 2024).

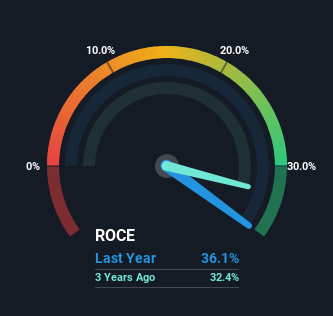

So, Nextracker has an ROCE of 36%. That’s a fantastic return and not only that, it outpaces the average of 13% earned by companies in a similar industry.

View our latest analysis for Nextracker

In the above chart we have measured Nextracker’s prior ROCE against its prior performance, but the future is arguably more important. If you’d like to see what analysts are forecasting going forward, you should check out our free analyst report for Nextracker .

What Can We Tell From Nextracker’s ROCE Trend?

The trends we’ve noticed at Nextracker are quite reassuring. The numbers show that in the last five years, the returns generated on capital employed have grown considerably to 36%. The amount of capital employed has increased too, by 331%. So we’re very much inspired by what we’re seeing at Nextracker thanks to its ability to profitably reinvest capital.

Our Take On Nextracker’s ROCE

A company that is growing its returns on capital and can consistently reinvest in itself is a highly sought after trait, and that’s what Nextracker has. And with a respectable 18% awarded to those who held the stock over the last year, you could argue that these developments are starting to get the attention they deserve. With that being said, we still think the promising fundamentals mean the company deserves some further due diligence.

Before jumping to any conclusions though, we need to know what value we’re getting for the current share price. That’s where you can check out our FREE intrinsic value estimation for NXT that compares the share price and estimated value.

Nextracker is not the only stock earning high returns. If you’d like to see more, check out our free list of companies earning high returns on equity with solid fundamentals.

Valuation is complex, but we’re helping make it simple.

Find out whether Nextracker is potentially over or undervalued by checking out our comprehensive analysis, which includes fair value estimates, risks and warnings, dividends, insider transactions and financial health.

View the Free Analysis

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we’re helping make it simple.

Find out whether Nextracker is potentially over or undervalued by checking out our comprehensive analysis, which includes fair value estimates, risks and warnings, dividends, insider transactions and financial health.

View the Free Analysis

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email [email protected]

Gregory Daniels is your guide to the latest trends, viral sensations, and internet phenomena. With a finger on the pulse of digital culture, he explores what’s trending across social media and pop culture. Gregory enjoys staying ahead of the curve and sharing emerging trends with his readers.